The Tokyo summer Olympics have been a welcome distraction over the last few weeks and well done to Japan for hosting the games so successfully in the current environment. In particular it is inspiring to see the years of preparation and planning being showcased by the top competitors in their respective sports, whether they are successful medallists or otherwise.

One common theme I observed when competitors were interviewed is the duration of the effort undertaken prior to the event, with training commencing for those with their sights on Paris 2024. The Olympic time horizon of four years is more comparable to what we think of as an appropriate period when investing on behalf of our clients. Tokyo 2020 showcased those at the top of their game. Similarly, the equity markets reflect companies that are, or are believed to be, today’s winners in the race for better profits. However, just as the list of competitors will change by the next Olympics, a mixture of returning stars and a healthy number of new or lesser-known names to discuss will be found in the equity markets of the future.

Our job as stock pickers is to find these future winners, the medallists of Paris in equity form. To explain what I think is the best approach I wanted to first highlight one Olympian, British shooter Seonaid McIntosh. She unfortunately didn’t make the medal podium but very much continued a remarkable tradition of target shooting in her family. With her mother and sister both Commonwealth games medallists and her father (also a successful shooter) a coach they clearly have something special as a family unit.

Source: Donald McIntosh

The reason I’m highlighting the McIntosh family is because I did my own 10,000 hours in target shooting whilst at university and beyond, with Seonaid’s parents as my teammates in many successful competitions. Whilst my personal successes pale compared to those of the McIntosh clan, they were at a level to realise, sometimes through painful experience, that having the right psychology is key to success when competing at higher levels in sport. I learnt during that period of my life that the best way to manage stressful competitions was to be extremely focused on just three key things and keep repeating them again and again. Complete focus on my chosen drills worked much better than dwelling on the possibility of winning or losing.

My suggestion is that this rule of three can very much be applied to investing in the equity markets. The three key drills our team always follows when choosing Future Quality companies are:

- High returns - Sustained high cash flow and returns on capital for growing companies should be targeted Every company we invest in has to have a strong franchise and management team that can deliver growth and sustain high returns on capital. Our long-standing holdings in Microsoft, TransUnion, and Progressive Corp are all good examples of companies that fit this bill. Over the last decade our portfolios overall have consistently had a skew towards higher returns on capital and superior revenue and earnings growth.

However, most companies are vulnerable to future competition, particularly when the returns on capital are high and/or the cost of capital is low. This latter point deserves particular focus today as in some parts of the market investors seem to be viewing the opportunities as a rather idyllic scene. If I had to use an analogy, it would be a scene of hot air balloons travelling in the morning sunshine.

Source: Shutterstock

These balloons could be branded as technology disruption, electric vehicles, GameStop or other currently popular themes, but we all know that as the day progresses these balloons will not stay high in the sky or travel particularly far unless they are refuelled by the arrival of profits. Our guess is that many will not see the latter scenario and the only debate will be the speed of their descent. Parts of the electric vehicle, internet, software and biotechnology sectors appear to be in the balloon category, primarily because they combine cheap capital (with the implications for future competition) and limited evidence of achieving high profitability over our required time horizon.

Which is why we are not in the business of travelling in hot air balloons and prefer instead a ground based journey where we are confident of travelling for further and longer. Because of our insistence on having a clear path to achieving and then sustaining high returns on invested capital over the next five years, we may miss out on some of today’s high-flyers. But experience tells us that we may also avoid the significant drawdowns that are so detrimental to compounding capital over the long term - Tail winds - Structural growth drivers can lead to several stock picks benefiting from a common theme Every company we invest in has to meet our Future Quality criteria on its own right and the collection of these ideas is what shapes the overall portfolio. However, there are often themes that are common to several companies that can make it easier for clients to understand why we have identified them as high conviction investments.

These themes often persist for many years, although investor optimism and the scale of positioning may mean that such long term prospects have already been discounted.

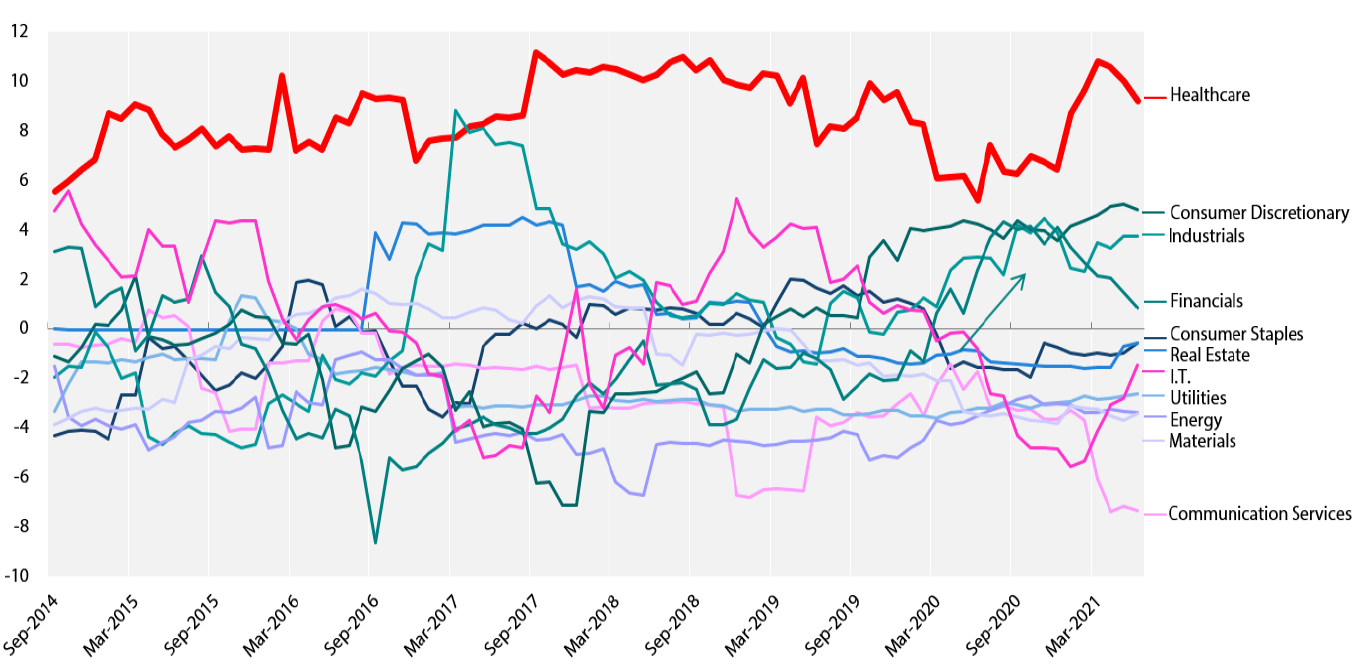

One theme we believe is both enduring and still underappreciated is linked to parts of the Healthcare sector. More specifically we are referring to those companies that are in a position to deliver the more cost-effective healthcare solutions that societies desire and need. This structural demand backdrop is a key element behind our high conviction in companies such as LHC, Encompass and Labcorp. The other area that excites us is the wave of innovation underway in areas such as gene therapy, with businesses such as Bio-Techne and Danaher providing the picks and shovels that enable this wave of innovation. These themes are a key element of why we have been notably overweight in the sector for much of the last decade.

Source: FactSet 1 September 2014–30 June 2021. Sector active weight uses Composite representative fund and benchmark MSCI ACWI ACWI-ex Australia Index from September 2014 to March 2016 and the MSCI ACWI Index from April 2016 to June 2021.

In more recent times we have become more enthused about a newer theme - the importance of energy transition - as societies realise that carbon emissions will have to be addressed much more proactively. This may not be a completely new story, but its materiality from an investment perspective has become more significant due to the following: 1) greater anecdotal and scientific evidence of global warming, 2) higher energy and carbon pricing, 3) governments using green solutions as a mechanism for economic stimulus and 4) asset owners favouring ESG solution providers and as result lowering the cost of capital.

Reference to individual stocks is for illustration purpose only and does not guarantee their continued inclusion in the strategy’s portfolio, nor constitute a recommendation to buy or sell.

Hydrogen in particular is at an exciting stage. This element with long-established technology has been prematurely hyped in the past, but it is now at a tipping point for demand acceleration as it is a component of meaningful CO2 reductions globally. Scale is key for the required cost reductions to make hydrogen more competitive, with the alternative being polluting energy sources. We are more confident that this is now being addressed due to more state sponsored projects, ramping of capacity and most importantly the falling cost and availability of renewable energy that is key to green hydrogen. - Improvement – Individual journeys of improving returns on capital are key to idiosyncratic alpha History tells us that most companies will not deliver very high returns on capital for prolonged periods. In particular, there is a quite low probability that companies can durably improve returns on capital from low or even average levels to being amongst the best in class. However, when companies do go on such a journey, they are often fantastic investments, and that is why we seek improving returns on capital whenever possible.

Many holdings within the portfolio have these characteristics but within the largest holdings there are a couple of companies that are excellent examples of that journey of improvement.

The first is HelloFresh, a global leader in the meal-kit market with a track record of taking market share from peers. For example, five years ago HelloFresh only had a 20% share of the US market, but the company’s share is now close to 60% due to its improvements in product, price and service. With a data-driven approach, HelloFresh enjoys a superior business model to its e-commerce peers. The company also has higher order rates, demand predictability and free cash flow conversion. Through a vertical integration of the supply chain and 90% of each box consisting of own-branded products, HelloFresh is able to capture a larger portion of the profit pool than traditional grocery retailers. This is resulting in sustained returns on invested capital exceeding 20%, although the company had been loss making as recently as 2019.

The second is Carlisle Companies, a more recent portfolio addition. Its management team is in the process of refocusing the company’s capital allocation by selling non-core businesses to concentrate investments in their core roofing business (70% of sales). We believe that there is significant pent up cyclical demand for their products, with commercial construction only now emerging from a long downturn. Re-roofing is also a source of increased energy efficiency and this should provide a more enduring tailwind for growth at the business. Since our purchase over the last quarter the firm has announced the acquisition of Henry Company, a leading provider of building envelope systems, which further increases our confidence of driving returns higher through greater business focus.

Inflation and (hopefully) educated guesses

We think it is really important to be honest about what we do and don’t know. The defence mechanism for many of those involved with managing money is to portray confidence on investment views, even when it is knowingly misplaced. The reality of investing is that we are attempting to make educated guesses about the future, which is not easy at the company level, and from our perspective even harder when addressing the dismal science of economic projections. The question of whether we will evolve to an inflationary regime or remain in a disinflationary one is the tough question we are now regularly asked….and in short, we don’t have a definitive answer.

The case for inflation rests on the willingness of central banks to undertake quantitative easing (QE) and more willingly finance (albeit not directly) sustainably higher fiscal deficits. With voters unlikely to accept austerity measures and with clear evidence of supply chain constraints we could see a structural shift to higher inflation expectations.

The case against however is that QE has failed to incite inflation over the last decade, supply constraints are temporary factors, debt burdens are now even greater and the disinflationary forces from the application of new technologies remain very strong.

Reference to individual stocks is for illustration purpose only and does not guarantee their continued inclusion in the strategy’s portfolio, nor constitute a recommendation to buy or sell.

Our working assumption is that the inflation headwinds will dominate for longer, a thesis that the collapse in bond yields in recent months would support. However, in the longer term the foundations for greater future inflation are becoming stronger. In short, a regime change (to higher inflation) may be underway but the pace of change is such that the economic cycle will still play second fiddle to the importance of seeking individual companies that can grow faster through market share gains or are in industries with superior growth prospects. But, as we suggested above, we will willingly adapt this guess if evidence supports a more rapid shift to an inflationary regime is indeed underway.

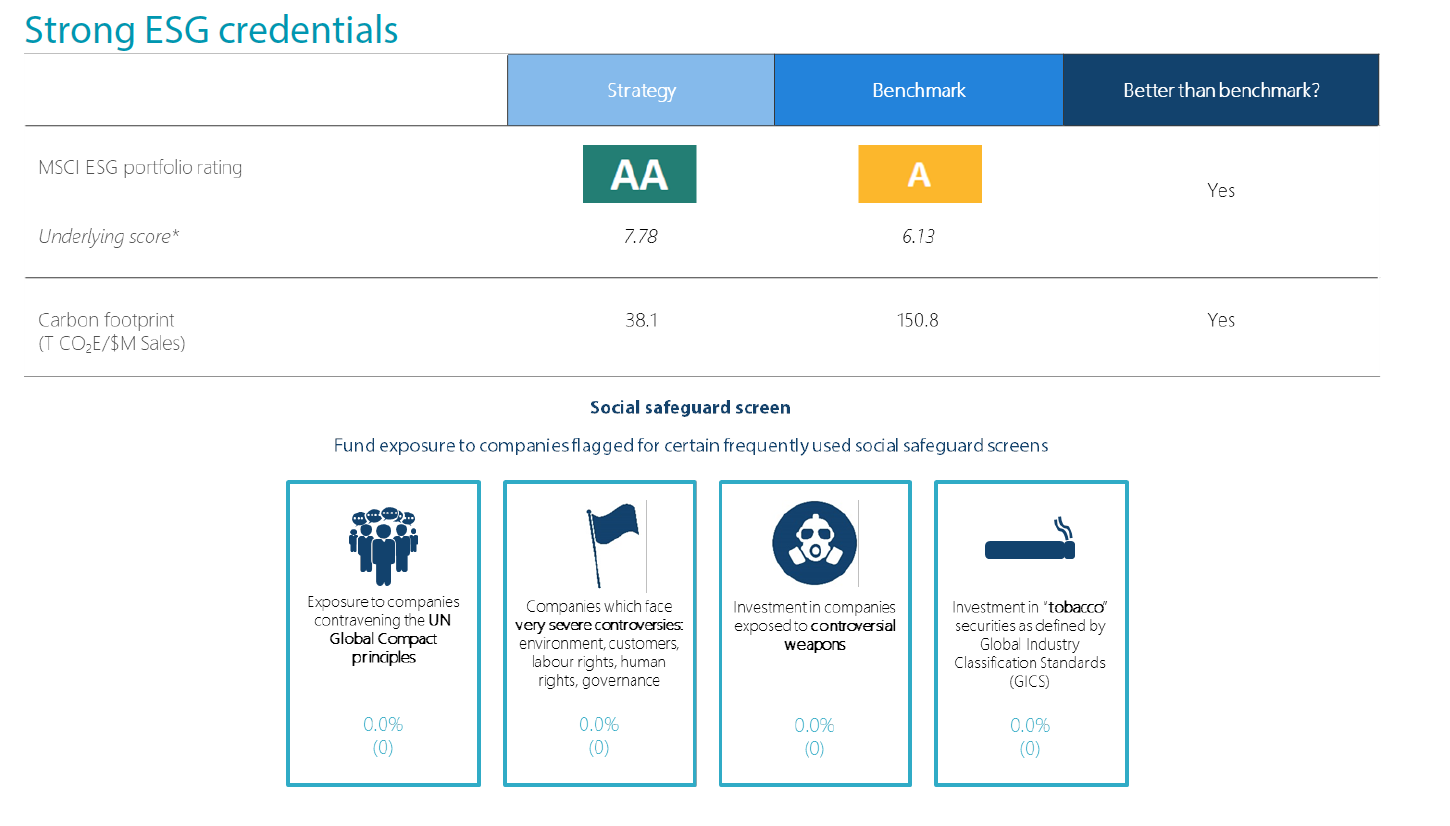

* Underlying score is the MSCI ESG Quality Score,. Carbon Footprint is Weighted Average Carbon Intensity Data supplied as per the MSCI definitions. Fund is a representative account of the Nikko AM Global Equity Strategy. Benchmark is the MSCI ACWI. Source: MSCI ESG Research June 2021

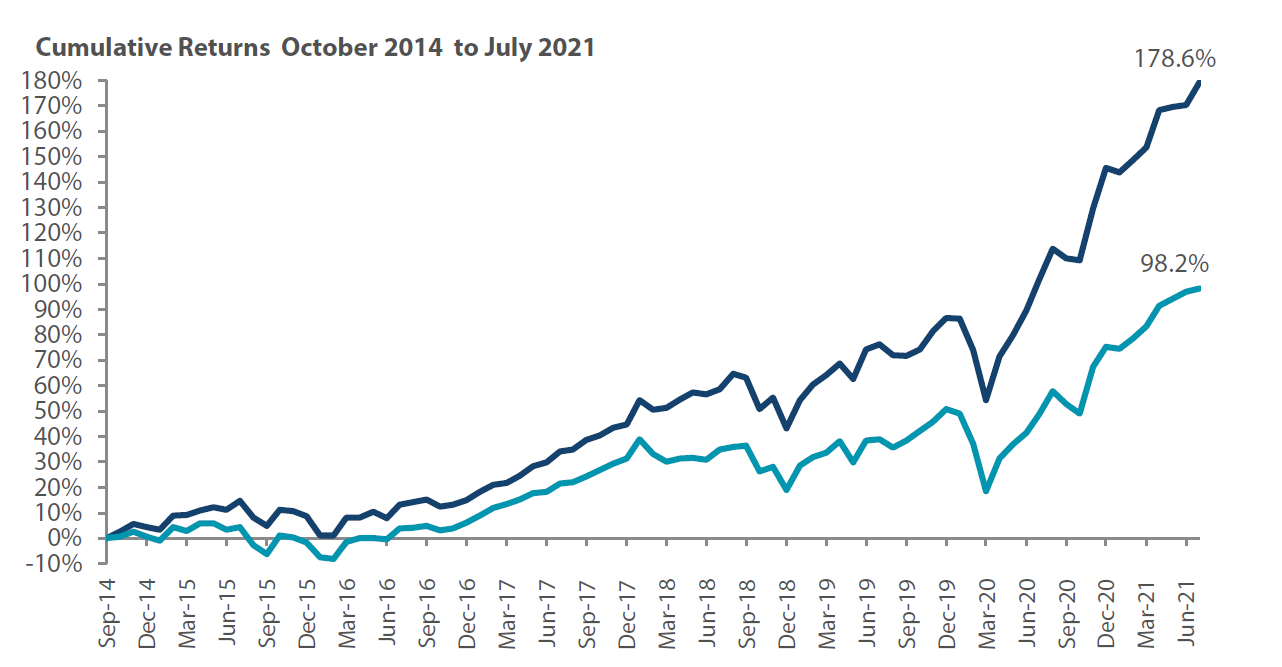

Global Equity Strategy Composite Performance to July 2021

*The benchmark for this composite is MSCI All Countries World Index. The benchmark was the MSCI All Countries World Index ex AU since inception of the composite to 31 March 2016. Inception date for the composite is 01 October 2014. Returns are based on Nikko AM’s (hereafter referred to as the “Firm”) Global Equity Strategy Composite returns. Returns for periods in excess of 1 year are annualised. The Firm claims compliance with the Global Investment Performance Standards (GIPS ®) and has prepared and presented this report in compliance with the GIPS. GIPS® is a registered trademark of CFA Institute. Returns are US Dollar based and are calculated gross of advisory and management fees, custodial fees and withholding taxes, but are net of transaction costs and include reinvestment of dividends and interest. Copyright © MSCI Inc. The copyright and intellectual rights to the index displayed above are the sole property of the index provider. For more details, please contact Nikko Asset Management. Any comparison to reference index or benchmark may have material inherent limitations and therefore should not be relied upon. Data as of 30 July 2021.

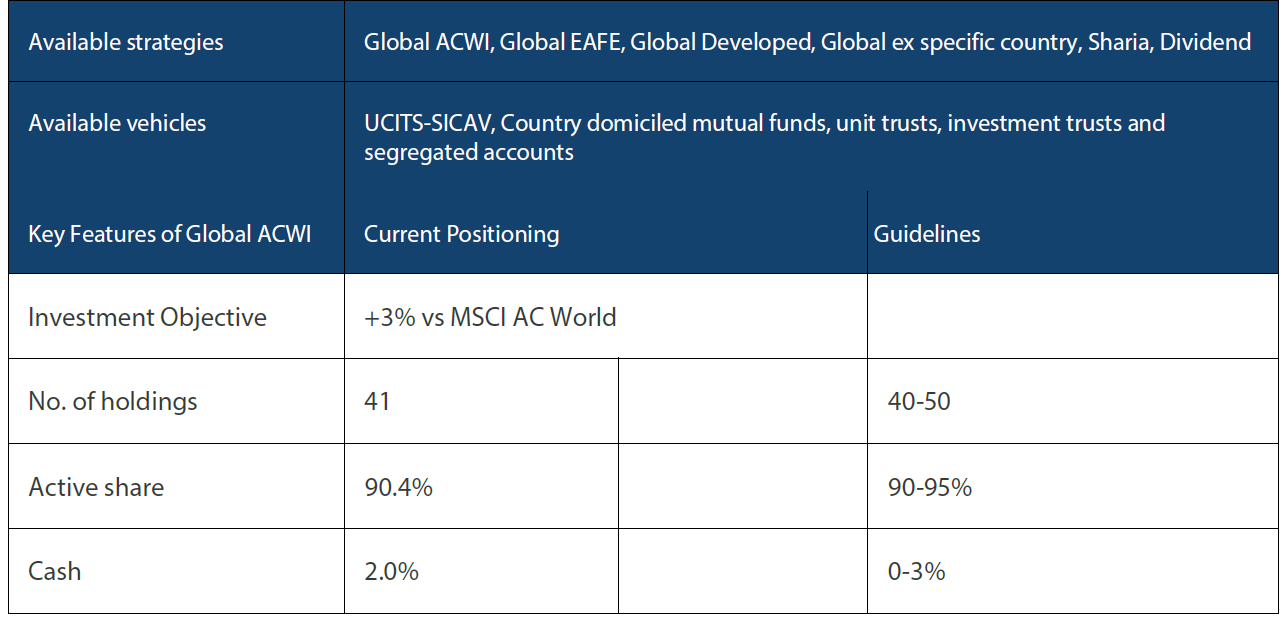

Nikko AM Global Equity: Capability profile and available funds (as at 30 July 2021)

Target return is an expected level of return based on certain assumptions and/or simulations taking into account the strategy’s risk components. There can be no assurance that any stated investment objective, including target return, will be achieved and therefore should not be relied upon. Past performance is not indicative of future performance. This is provided as supplementary information to the performance reports prepared and presented in compliance with the Global Investment Performance Standards (GIPS®). GIPS® is a registered trademark of CFA Institute. Nikko AM Representative Global Equity account. Source: Nikko AM, FactSet.