.jpg?width=754&name=iStock-1150017950%20(1).jpg)

Another quarter goes by and we are still (in the United Kingdom anyway) limited in our ability to travel and congregate in offices. In my spare time, I often end up searching vainly for fresh and interesting new content, only to revert to watching stalwarts such as the Bourne film series.

It’s interesting to observe how technology has evolved since these movies were released and how Hollywood’s portrayal of tracking people’s locations has quickly become a reality for us all. What I also found interesting was the appeal of not knowing what’s next and being taken on an unexpected journey.

While the unexpected makes for gripping viewing, equity investors are looking for the exact opposite. They want to know where they are headed at the outset and would prefer to avoid twists and turns in their investment journey. 2020 however, has been more like a Hollywood script, with a myriad of plot twists such as COVID and the US election cycle. These unexpected twists have also been what every newscaster and by default many investors, have anchored around. The number of expert political pundits or epidemiologists seems to have proliferated massively.

In the physical world, knowing where you are going has evolved incredibly over the recent centuries from the invention of the sextant in the 1700s to today’s world where GPS allows our exact location to be measured in centimetres. We can now model with precision the forecasts for long-term profitability of every company we invest in and subject to these inputs, a fair valuation of the business. This precision is hugely helpful in assessing the investment case. But the subjective elements of our inputs are vulnerable to what’s happening in the current environment, which can encourage myopia and a major dose of recency bias.

The reality of being blown way off course by these unexpected events is that navigation can feel like using a sextant rather than a GPS to plot your course.

Future Quality Insights

Our GPS in such times has been our Future Quality philosphy. We always start our journey as shareholders confident that the business we invest in will be a strong franchise delivering high returns on capital; that is has a management team we can trust, and a strong balance sheet to weather both the good and bad times ahead. These credentials have proven their worth when unexpected situations such as the COVID-19 crisis emerge.

The journey involves investing in growing companies that we believe will attain and sustain high returns on invested capital. This includes those can beat the odds of high returns fading back towards the cost of capital and also those that are on a path to higher returns on capital, which the market does not yet recognise. When the path gets confused, as it has been by the COVID-19 situation and, to a lesser extent by the political shennanigans, we just keep reviewing whether the logic and forecasts we started with are still relevant and the case Future Quality is still there.

We have talked extensively about the quality metrics we seek in prior insights and these change little quarter to quarter. The focus therefore in this update is on the following key questions we have been asking on every company in our portfolios.

- Are returns improving? The trajectory of future returns is key to superior share price returns and this is what excites us when we research companies. Over a minimum of the next five years, a company has to grow and either sustain very high returns on capital or be on a path to these higher returns. When investors recognise that a company is on such a path, the outcome for shareholders tends to be rather good.

- Is the valuation attractive or expensive? Having a long-term horizon (over five years) when assessing businesses—a longer duration than the majority of market participants—we are quite comfortable if there is a premium valuation from a historical perspective. This “premium” quickly disappears when there is a subsequent delivery of superior growth and high or typically improving returns on capital. However, this discounting of future profits by the market can vary by both the duration and degree of optimism, and if the valuation already factors in a best case outcome, it should be a catalyst to sell in favour of better alternatives.

We believe that investing in Future Quality companies will lead to outperformance over the full market cycle. Our strategy is based on fundamental, bottom-up research therefore sector and country allocations are a function of stock selection. The Global Equity strategy is a concentrated, high conviction portfolio with a high active share ratio.

Investing for improving returns in a COVID-19 world

To state the obvious, 2020 has turned out to be annus horribilis for many. Even well managed businesses have been caught on the wrong side of the work from home/out of home divide. Forced acquaintance with a home desk, video communication technology, and a hiatus in commuting have imposed change on everyone. In particular, this has accelerated a variety of structural trends already in place, bringing forward growth and profitability for many of our key holdings. The following holdings (~60% of the portfolio) are benefitting from these broader and accelerating structural trends:

- Gaming Nintendo, Tencent, Sony.

- Cloud adoption Microsoft, Adobe, Accenture, Amazon.

- Healthcare solution providers LHC, Philips, Anthem, LabCorp, Danaher, Bio-Techne, LivaNova, Encompass Health.

- Home delivery Meitaun Dianping, HelloFresh, Amazon.

- Power of data analysis TransUnion, Verisk, AON, Palomar, Progressive.

Putting valuation to one side (we will discuss later) the superior quality and growth metrics of these businesses will likely remain. They are still on the path we seek, albeit travelling at a quickened pace.

However, the COVID-19 world is very much about winners and losers and hence the intense focus for most investors on vaccines, a normalisation of activity and the hope for rebound in profitability. We have never pretended to be epidemiologists, but have remained comfortable that a rebound in activity would indeed occur over time. Before this can occur, markets will have to keep addressing the following challenges:

- The globalisation wave is over as China moves towards domestic priorities and the battle of global technology leadership continues. Freedom of movement for trade and capital will become more restrictive, with politicians defining the pace of this change.

- Higher unemployment in societies with high inequalities is a troublesome cocktail, and governments will do everything in their power to support businesses and create employment. Zombie businesses will continue to operate in many industries and be a hindrance to future pricing power.

- Growing government debt burdens can only be supported if borrowing costs remain suppressed by quantitative easing. This will make the yield curve a poor profit source for many financial businesses and those countries unable to undertake this QE yield management will be relative losers.

On the winning side of the ledger will be the prospects for greater spending by governments on the environmental challenges we all face. In our view, the ‘green deal’ will become the real deal. Hence we see significant opportunities for the businesses that solve these challenges with the right products and solutions for a growing client base. We believe our holdings in Daikin, Kingspan, Schneider, SolarEdge, Johnson Matthey, Woodward and Deere & Co are all beneficiaries of these trends.

Looking through the COVID-19 cycle we do see demand gradually returning to pre- COVID-19 levels over time, albeit with the duration varying considerably between the extremes of airline operators and used car garages, the latter benefitting from an enduring wariness in using public transport in the West. Our constant focus on high cash flow returns and strong balance sheets makes us confident that our companies with COVID-19 headwinds will be the survivors set to benefit from the recovery when it does occur. Our current research focus is on trying to assess whether investors’ expectations of a normalisation in activity for COVID-19 impacted companies are too quick or too slow.

Above all else though, the path of improving returns on capital is invariably unique to each company and this is the attribute we most focus on when researching the companies we invest in. Any thematic explanation of portfolio positioning is just the aggregation of individual high conviction investment ideas.

Valuation dispersions – time to reassess?

Valuation is one of the key pillars that all of our holdings have to meet to be deemed Future Quality. We forecast future growth, profitability and cash flows for the next five years (as a minimum) for the businesses we invest in. These forecasts drive the valuation models we use when analysing each business and they are used to assess whether a supporting valuation pillar is in place. For most investors, valuation is anchored around historical metrics of profitability and as a result the virtues of compounding better growth and high or improving returns on capital are often missed by those focused on available backward looking quantitative measures. Hence we have always been relaxed about paying a premium for the higher quality businesses we invest in, as this premium is typically proven to be illusory by the delivery of subsequent cash flow generation.

The reaction of central banks to the COVID-19 situation has been to inject significant liquidity into financial systems through the use of quantitative easing, and to indicate that they will do more of the same as required. For those countries able to undertake such measures, investors have quite rationally assumed an enduringly lower cost of risk-free capital. This is the key factor supporting overall equity market valuations as we believe the real returns from alternative asset classes such as cash or government bonds are derisory and unlikely to solve the return targets of most asset owners.

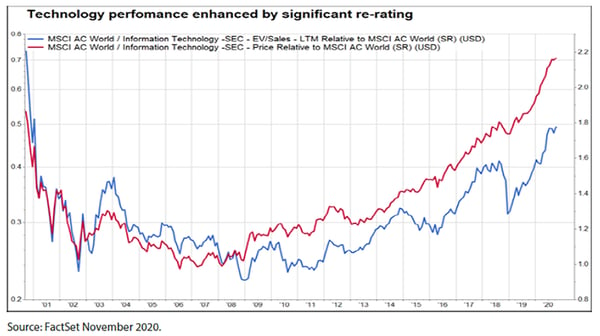

However, this rational explanation for overall market valuations becomes more uncomfortable when assessing the fair price for individual companies. Investors have continued to seek companies where there is high confidence of superior growth and profitability, with some larger cap technology or consumer Internet businesses being notable examples. This is the rational part. The less rational part is the desire for some investors to ‘rent’ parts of the market that are deemed more attractive for now. This attractiveness appears to have become more superficial, with thematics and momentum encouraging participation, particularly by retail investors, whilst the fundamentals such as making profits or generating cash flow have been glossed over for now. For those who have invested through multiple periods of market exuberance and panic, there is now too much exuberance in some pockets of the market, and this is primarily in the technology sector.

Chart 1: Technology performance enhanced by significant re-rating

Source: FactSet November 2020.

Where high share price returns have been dominated by higher valuations rather than improvements in future profitability, we have been reviewing the investment case. Within our investment process this is flagged in a disciplined way by our stock ranking tool. As a company’s rank declines, we adjust weightings in favour of better alternatives or may sell completely in favour of better new ideas. Over the last few months (as Chart 2 highlights) this has resulted in lower weights in technology companies.

Chart 2: Information technology active weight

Source: Nikko AM, FactSet 30 September 2020

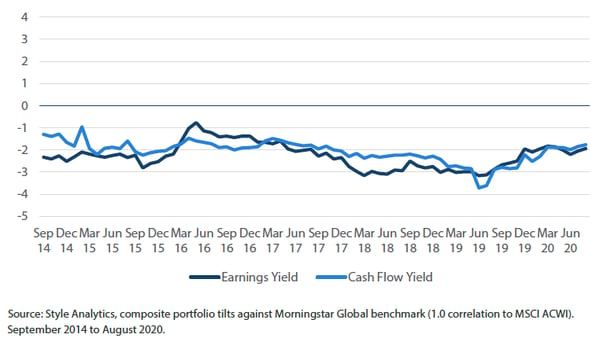

At the total portfolio level our historical valuation premium has been maintained at appropriate levels. We look to deliver compound returns for investors and being disciplined about our valuation pillar plays a key part in that.

Chart 3 Composite tilt versus benchmark

Source: Style Analytics, composite portfolio tilts against Morningstar Global benchmark (1.0 correlation to MSCI ACWI). September 2014 to August 2020.

As part of this process, we have added two new holdings over the last few months that we believe are good examples of where we see Future Quality with the valuation pillar being in place.

Deere & Co – Technology adoption is a key driver in many industries, as is the case for Deere & Co, the leading provider of agricultural equipment in the US market. This business is moderately cyclical, albeit is now entering an upcycle as the existing ageing fleet requires replacement. What is more interesting is the increased focus on delivering technology solutions for precision agriculture, which we believe will enhance margins from a structural perspective. This, combined with ongoing cost efficiencies will result in returns on capital being less cyclical and to endure at levels that meet our Future Quality thresholds.

Encompass Healthcare – Whilst COVID-19 has dominated healthcare headlines the unfortunate reality remains that other diseases are ever present and the need for high quality and cost-effective care in ageing society is as great as ever. Encompass Health is the largest provider in Inpatient Rehabilitation Facilities (IRFs) in the US and if you are unlucky enough to have a stroke or other acute issues you will value their quality care either as an inpatient or via home health. The focus on COVID-19 beneficiaries by investors has left the longer-term growth prospects of this industry leader ignored in our view.

Being prepared for change

Assessing prior strong market returns is a dilemma we need to address for clients, but it does leave this writer with an uncomfortable feeling that we are doing so in an almost surreal and rather unfair environment. Financial market participants and owners of capital have been the clear winners post the GFC and the same playbook is unfolding in this current crisis. My personal view is that this is not a fair outcome and it is only a matter of time before greater societal backlashes emerge against this. What form this will take and its timing is a significant unknown, but we need to be prepared for changes to the rules of the game. Being pragmatic, willing to accept change and having an investment philosophy that is agnostic to whatever path politicians take us down will be key to being good stewards of client’s capital in the coming years.

Reference to individual stocks is for illustration purpose only and does not guarantee their continued inclusion in the strategy’s portfolio, nor constitute a recommendation to buy or sell.

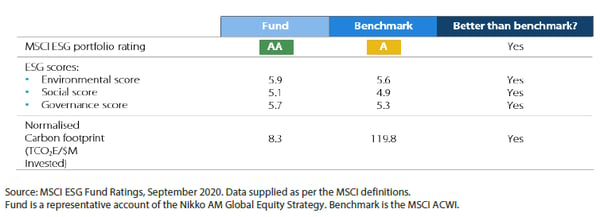

Strong ESG credentials

Source: MSCI ESG Fund Ratings, September 2020. Data supplied as per the MSCI definitions. Fund is a representative Nikko AM Global Equity Strategy. Benchmark is the MSCI ACWI.

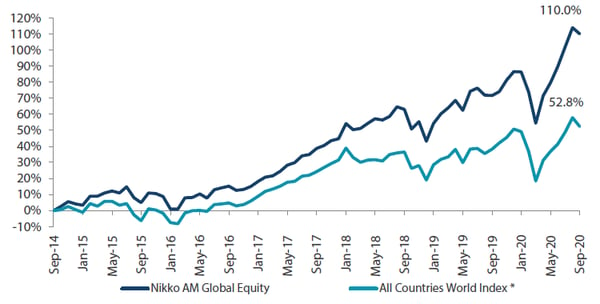

Global Equity Strategy Composite Performance to Q3 2020

*The benchmark for this composite is MSCI All Countries World Index. The benchmark was the MSCI All Countries World Index ex AU since inception of the composite to 31 March 2016. Inception date for the composite is 01 October 2014. Returns are based on Nikko AM’s (hereafter referred to as the “Firm”) Global Equity Strategy Composite returns. Returns for periods in excess of 1 year are annualised. The Firm claims compliance with the Global Investment Performance Standards (GIPS ®) and has prepared and presented this report in compliance with the GIPS. Returns are US Dollar based and are calculated gross of advisory and management fees, custodial fees and withholding taxes, but are net of transaction costs and include reinvestment of dividends and interest. Copyright © MSCI Inc. The copyright and intellectual rights to the index displayed above are the sole property of the index provider. For more details, please refer to the performance disclosures found at the end of this document. Any comparison to reference index or benchmark may have material inherent limitations and therefore should not be relied upon. Data as of 30 September 2020.

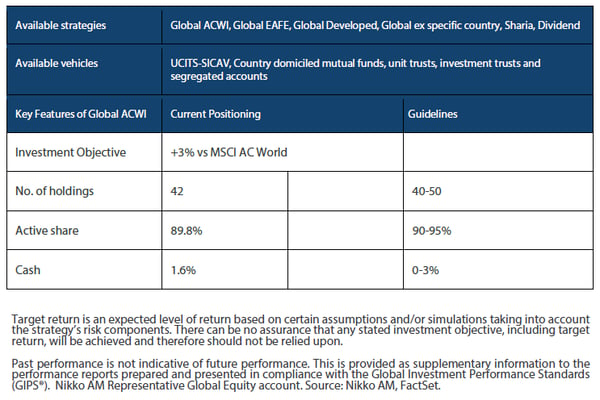

Nikko AM Global Equity: Capability profile and available funds (as at 30 September 2020)

Target return is an expected level of return based on certain assumptions and/or simulations taking into account the strategy’s risk components. There can be no assurance that any stated investment objective, including target return, will be achieved and therefore should not be relied upon.

Past performance is not indicative of future performance. This is provided as supplementary information to the performance reports prepared and presented in compliance with the Global Investment Performance Standards (GIPS®). Nikko AM Representative Global Equity account. Source: Nikko AM, FactSet.

Nikko AM Global Equity Team

This Edinburgh based team provides solutions for clients seeking global exposure. Their unique approach, a combination of Experience, Future Quality and Execution, means they are continually “joining the dots” across geographies, sectors and companies, to find the opportunities that others simply don’t see.

Experience

Our five portfolio managers have an average of 23 years’ industry experience and have worked together as a Global Equity team for eight years. In 2019, two portfolio analysts, Michael Chen and Ellie Stephenson joined the team and they are the first in a new generation of talent on the path to becoming portfolio managers. The team’s deliberate flat structure fosters individual accountability and collective responsibility. It is designed to take advantage of the diversity of backgrounds and areas of specialisation to ensure the team can find the investment opportunities others don’t.

Future Quality

The team’s philosophy is based on the belief that investing in a portfolio of Future Quality companies will lead to outperformance over the long term. They define Future Quality as a business that can generate sustained growth in cash flow and improving returns on investment. They believe the rewards are greatest where these qualities are sustainable and the valuation is attractive. This concept underpins everything the team does.

Execution

Effective execution is essential to fully harness Future Quality ideas in portfolios. We combine a differentiated process with a highly collaborative culture to achieve our goal: high conviction portfolios delivering the best outcome for clients. It is this combination of extensive experience, Future Quality style and effective execution that offers a compelling and differentiated outcome for our clients.

About Nikko Asset Management

With USD 249.5 billion* under management, Nikko Asset Management is one of Asia’s largest asset managers,

providing high-conviction, active fund management across a range of Equity, Fixed Income, Multi-Asset and Alternative strategies. In addition, its complementary range of passive strategies covers more than 20 indices and includes some of Asia’s largest exchange-traded funds (ETFs).

*Consolidated assets under management and sub-advisory of Nikko Asset Management and its subsidiaries as of 30 September 2020.

Risks

Emerging markets risk - the risk arising from political and institutional factors which make investments in emerging markets less liquid and subject to potential difficulties in dealing, settlement, accounting and custody.

Currency risk - this exists when the strategy invests in assets denominated in a different currency. A devaluation of the asset's currency relative to the currency of the Sub-Fund will lead to a reduction in the value of the strategy.

Operational risk - due to issues such as natural disasters, technical problems and fraud.

Liquidity risk - investments that could have a lower level of liquidity due to (extreme) market conditions or issuer-specific factors and or large redemptions of shareholders. Liquidity risk is the risk that a position in the portfolio cannot be sold, liquidated or closed at limited cost in an adequately short time frame as required to meet liabilities of the Strategy.

Important Information: This document is prepared by Nikko Asset Management Co., Ltd. and/or its affiliates (Nikko AM) and is for distribution only under such circumstances as may be permitted by applicable laws. This document does not constitute personal investment advice or a personal recommendation and it does not consider in any way the objectives, financial situation or needs of any recipients. All recipients are recommended to consult with their independent tax, financial and legal advisers prior to any investment.

This document is for information purposes only and is not intended to be an offer, or a solicitation of an offer, to buy or sell any investments or participate in any trading strategy. Moreover, the information in this document will not affect Nikko AM’s investment strategy in any way. The information and opinions in this document have been derived from or reached from sources believed in good faith to be reliable but have not been independently verified. Nikko AM makes no guarantee, representation or warranty, express or implied, and accepts no responsibility or liability for the accuracy or completeness of this document. No reliance should be placed on any assumptions, forecasts, projections, estimates or prospects contained within this document. This document should not be regarded by recipients as a substitute for the exercise of their own judgment. Opinions stated in this document may change without notice.

In any investment, past performance is neither an indication nor guarantee of future performance and a loss of capital may occur. Estimates of future performance are based on assumptions that may not be realised. Investors should be able to withstand the loss of any principal investment. The mention of individual securities, sectors, regions or countries within this document does not imply a recommendation to buy or sell.

Nikko AM accepts no liability whatsoever for any loss or damage of any kind arising out of the use of all or any part of this document, provided that nothing herein excludes or restricts any liability of Nikko AM under applicable regulatory rules or requirements.

All information contained in this document is solely for the attention and use of the intended recipients. Any use beyond that intended by Nikko AM is strictly prohibited.

New Zealand: This document is issued in New Zealand by Nikko Asset Management New Zealand Limited (Company No. 606057, FSP22562). It is for the use of wholesale clients, researchers, licensed Financial Advice Providers (FAP) and their authorised representatives only.

Disclaimer: Nikko Asset Management New Zealand Limited (Company No. 606057, FSP22562) is the licensed Investment Manager of Nikko AM NZ Investment Scheme, Nikko AM NZ Wholesale Investment Scheme and the Nikko AM KiwiSaver Scheme. This material has been prepared without taking into account a potential investor’s objectives, financial situation or needs and is not intended to constitute personal financial advice, and must not be relied on as such. The Product Disclosure Statements are available on our website: https://www.nikkoam.co.nz./invest/retail